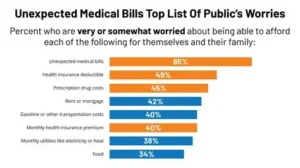

In the United States, a single medical emergency can cost more than a luxury car — sometimes even more than a house down payment.

In 2026, hospital stays, surgeries, and specialty treatments can easily cross $50,000 to $100,000 without proper insurance coverage. For many American families, medical debt remains one of the leading causes of bankruptcy.

This guide explains how to financially protect yourself using the right health insurance strategy, tax planning tools, and risk management techniques.

1. Why Medical Bills Are So High in America

Healthcare costs in the U.S. are driven by:

- Advanced medical technology

- High specialist wages

- Administrative overhead

- Expensive prescription drugs

- Private hospital pricing power

Even insured patients may face:

- High deductibles

- Coinsurance

- Out-of-pocket maximum exposure

Without proper planning, costs can escalate quickly.

2. Choosing the Right Health Insurance Plan in 2026

Plans regulated under the Affordable Care Act offer structured coverage options through federal and state marketplaces.

Key plan tiers:

- Bronze (low premium, high deductible)

- Silver (balanced coverage)

- Gold (higher premium, lower out-of-pocket)

- Platinum (maximum coverage)

Your ideal plan depends on:

- Expected medical usage

- Family size

- Income level

- Risk tolerance

High-income households often optimize between premium savings and tax advantages.

3. The Power of Health Savings Accounts (HSA)

A Health Savings Account (HSA) is one of the most powerful tax-advantaged tools available in the U.S.

Benefits include:

- Pre-tax contributions

- Tax-free growth

- Tax-free withdrawals for medical expenses

When combined with a high-deductible health plan (HDHP), HSAs can significantly reduce lifetime healthcare costs.

Many financial advisors treat HSAs as a “stealth retirement account” due to triple tax benefits.

4. Medical Debt & Bankruptcy Risk

Medical debt remains a top driver of personal bankruptcy filings in America.

Protection strategies include:

- Selecting appropriate out-of-pocket maximums

- Maintaining emergency savings (6–12 months expenses)

- Supplemental insurance policies

- Critical illness coverage

Proper coverage prevents financial catastrophe.

5. Employer Plans vs Marketplace Plans

Employer-sponsored coverage often offers:

- Group-negotiated pricing

- Lower premiums

- Payroll deduction convenience

Marketplace plans offer:

- Subsidy eligibility

- Greater portability

- Customization options

Eligibility for premium tax credits depends on income thresholds under the Affordable Care Act.

6. How Credit & Income Impact Healthcare Financing

While health insurance pricing is regulated, medical debt can affect:

- Credit scores

- Loan approvals

- Mortgage eligibility

Financial planning around healthcare reduces long-term borrowing risk.

7. High-Income Professionals: Advanced Protection Strategies

Doctors, lawyers, business owners, and tech professionals often consider:

- Private PPO plans

- Supplemental gap coverage

- Disability insurance

- Long-term care insurance

- Medical liability coverage

These policies protect both income and assets.

8. Telehealth & Cost Reduction in 2026

Digital healthcare platforms reduce:

- Emergency room visits

- Minor care expenses

- Consultation costs

Telehealth adoption lowers insurer claim frequency, helping moderate premium growth.

9. How AI Is Reducing Insurance Fraud

Major insurers now use artificial intelligence to detect:

- Billing anomalies

- Duplicate claims

- Provider fraud

- Inflated procedure coding

Companies like UnitedHealth Group and Elevance Health are investing heavily in AI-driven cost control systems.

Lower fraud improves long-term pricing stability.

10. Smart Financial Checklist for 2026

✔ Compare plans annually

✔ Maximize HSA contributions

✔ Understand deductible vs premium trade-offs

✔ Check provider network coverage

✔ Maintain emergency fund

✔ Review out-of-pocket maximum

✔ Evaluate supplemental coverage

Small decisions can save tens of thousands of dollars over time.

11. Will Health Insurance Premiums Keep Rising?

Premiums are influenced by:

- Medical inflation

- Drug pricing

- Aging demographics

- Regulatory changes

- Reinsurance markets

While cost pressures remain, technology, transparency, and AI-driven efficiency may slow growth over time.

Final Thoughts: Protecting Your Financial Future

Healthcare costs in America are unlikely to fall dramatically. However, smart insurance planning, tax optimization, and risk management can prevent six-figure medical disasters.

Health insurance in 2026 is not just about compliance — it is about wealth protection.

A well-structured coverage strategy ensures that a medical emergency does not become a financial emergency.